You can become a reporting group either automatically through control or through election.

Becoming a reporting group with your business group

This section refers to the Act sections 10A(1)(a) and (3) and 11, and Rules section 2–1(1) and (2)(a-c).

Control is the main principle to the existence of business groups. You're in a business group if your business is in a control structure. This is where one person controls one or more persons.

To determine if you’re a business group, you must consider if you’re within a control structure. You won’t be in a business group unless a control relationship exists.

Learn more about determining control.

Determining if you’re in a business group

This section refers to the Rules section 2–1(1) and (1A) and Explanatory Statement 62.

Your first step is to determine if you’re in a business group, which requires you to determine the control structure of the businesses in your group.

To determine your control structure and members, start by asking, is your business part of a wider business group structure, where one or more persons are controlled by another?

If you answered ‘yes’, you’re in a business group. Your group will include the following persons as members:

- your business

- the person who controls the other persons in the group

- all the persons who this person controls.

Learn more about determining control.

How a business group becomes a reporting group

Your business group will automatically be a reporting group if one or more persons in the group provide a designated service

The members of the reporting group will then be all persons within the business group.

Example: Your business provides designated services and is a subsidiary of a parent company (which doesn’t provide designated services). The parent company is also a subsidiary of an ultimate holding company that doesn’t provide designated services.

Your parent company controls other persons, some of which provide designated services.

Your reporting group will consist of:

- your business and the parent company

- the ultimate holding company

- all other persons in the same control structure.

Choosing the lead entity

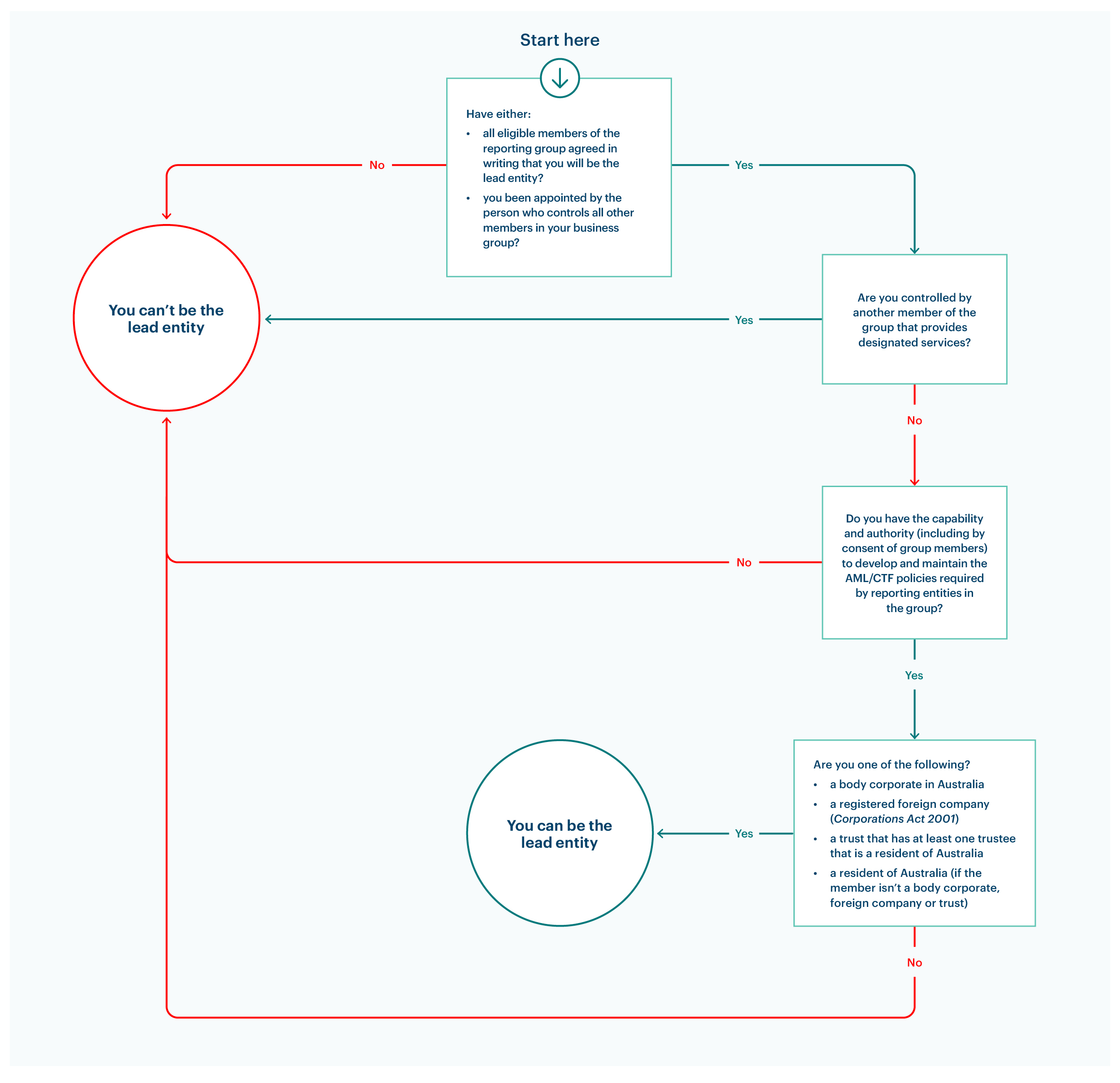

Your reporting group must have a lead entity in place within 28 days. Your reporting group will cease to exist if a lead entity has not been selected within this time.

Your business group can’t be split into more than one reporting group. It becomes one reporting group, with all members within the business group.

The lead entity must be chosen by either of the following ways:

- the person that controls all members of the group appoints the lead entity in writing

- each eligible member in your business group, agrees in writing on the lead entity.

The lead entity must also both:

- not be controlled by another member that provides a designated service

- have the required connection to Australia.

Having the required connection to Australia means that they’re one of the following:

- an Australian resident

- a body corporate incorporated in Australia

- a registered foreign company (within the meaning of the Corporations Act 2001)

- a trust that has at least one trustee that’s a resident of Australia.

Your lead entity must have the authority and capability to develop and maintain the anti-money laundering and counter-terrorism financing (AML/CTF) policies of the reporting entities in the group.

You can’t be a reporting group with only some of the members of the business group. All must be included in the reporting group.

Learn about the role of lead entities.

Opting out

This section refers to the Rules section 2–1(1).

Your business group won’t be a reporting group if either:

- no lead entity is in place within 28 days

- a reporting entity in the group opts out, in writing.

To opt out, you must be a reporting entity in your business group and do all the following:

- give all reporting entities, including the lead entity) in the business group written notice that you don’t want to be a member of the reporting group

- not withdraw the written notice

- continue to be a reporting entity.

You must ensure that you take reasonable steps to give written notice to the other reporting entities. Reasonable steps will depend on the nature, size and complexity of your business group.

If you’re already on the Reporting Entities Roll, you must advise of changes to your enrolment details.

This includes updating your membership status in a reporting group.

Forming elective reporting groups

This section refers to the Act section 10A(1)(b).

An elective reporting group can form when 2 or more reporting entities agree to do so. A business group can also join an elective reporting group, but all members of the business group must join.

Election process and eligibility

This section refers to the Act sections 10A(1)(b)(i and iii) and the Rules sections 2–2(1)(a–c), (3)(b), (4), (5), (7), (8), (9) and (10)(a).

To form an elective reporting group each of your members must both:

- elect in writing to be a member of the group

- not be a member of another elective group.

Members in your elective reporting group must be one or more of the following:

- a reporting entity

- a person who discharges AML/CTF obligations on behalf of another member

- all of the members of a business group.

Once formed, all members in your elective reporting group (including the member being elected as lead entity) must:

- agree on a lead entity

- make sure that your group doesn’t operate without a lead entity for more than 28 days.

Learn more about the role of lead entity.

When you join or leave an elective reporting group there are requirements you must meet. This includes:

- getting the lead entity’s consent to join an existing elective reporting group

- providing written notice to the lead entity when you leave the group

- if you’re the lead entity, providing written notice to your members when you leave.

If you are in a business group that is in an elective reporting group, then the whole business group must join or leave together.

Business group members joining an elective reporting group

This section refers to the Rules sections 2–2(1)(c), (2), (5–6), (9) and (11).

This may be useful to larger businesses who share operations with entities outside of their control structure.

You can elect to join or leave an elective reporting group if you’re a member of a business group. However, all the members of your business group must also join or leave with you.

If any business group member has opted out, the remaining members of your business group can’t join an elective reporting group.

For example, if you join an elective reporting group and are a member of a business group, all persons in your business group must join with you. If you leave the elective group, then all members of your business group must leave with you.

You can join an elective reporting group if both:

- another member of your business group elects to join on behalf of all members

- each member of your business group agrees to join.

We’ll consider you as a member of the elective reporting group only if you’re a member of both:

- an elective group

- a business group

The role of lead entity

This section refers to the Act sections 26F(5–6) and 10A(5), the Rules sections 2–1(2)(b and d) and 2–2(3)(a and d) and Explanatory Memorandums 46, 51, 53 and 56.

Your reporting group must have a lead entity.

Your lead entity is the person responsible for group-wide AML/CTF compliance. This includes:

- ensuring the appropriate sharing of information between members

- the creation and maintenance of the group-wide ML/TF risk assessment

- the creation and maintenance of group-wide AML/CTF policies which can be tailored to individual reporting entities in the group

- oversight and management of members’ AML/CTF compliance

- management of ML/TF risks.

Your lead entity acts as the central point of accountability for your reporting group’s compliance under the Act. If you’re a member that’s a reporting entity, you’re also directly accountable for compliance with the Act for the designated services you provide.

Whilst lead entities of business and elective reporting groups differ, they share common requirements. The lead entities in both types of reporting groups must both:

- not be controlled by another member that provides a designated service

- have the required connection to Australia.

Reporting groups that are business groups

This section refers to the Rules sections 2–1(1), (2)(a-d).

Your reporting group must have a lead entity within 28 days of becoming a reporting group. This can be done if either:

- the person who controls all members in your business group appoints the lead entity

- all eligible members in your business group agree in writing.

Eligible members are the members in your business group who are both:

- not controlled by another reporting entity

- have the required connection to Australia.

A lead entity must either have the authority, including by consent, and be capable to both:

- develop AML/CTF policies for the group

- maintain AML/CTF policies for the group.

A lead entity must also both:

- not be controlled by another reporting entity

- be an Australian-based member.

The flowchart below will help you decide if you can be a lead entity of your reporting group. If your answers lead you to ‘you can’t be the lead entity’, we recommend restarting the process.

Can I be a lead entity?

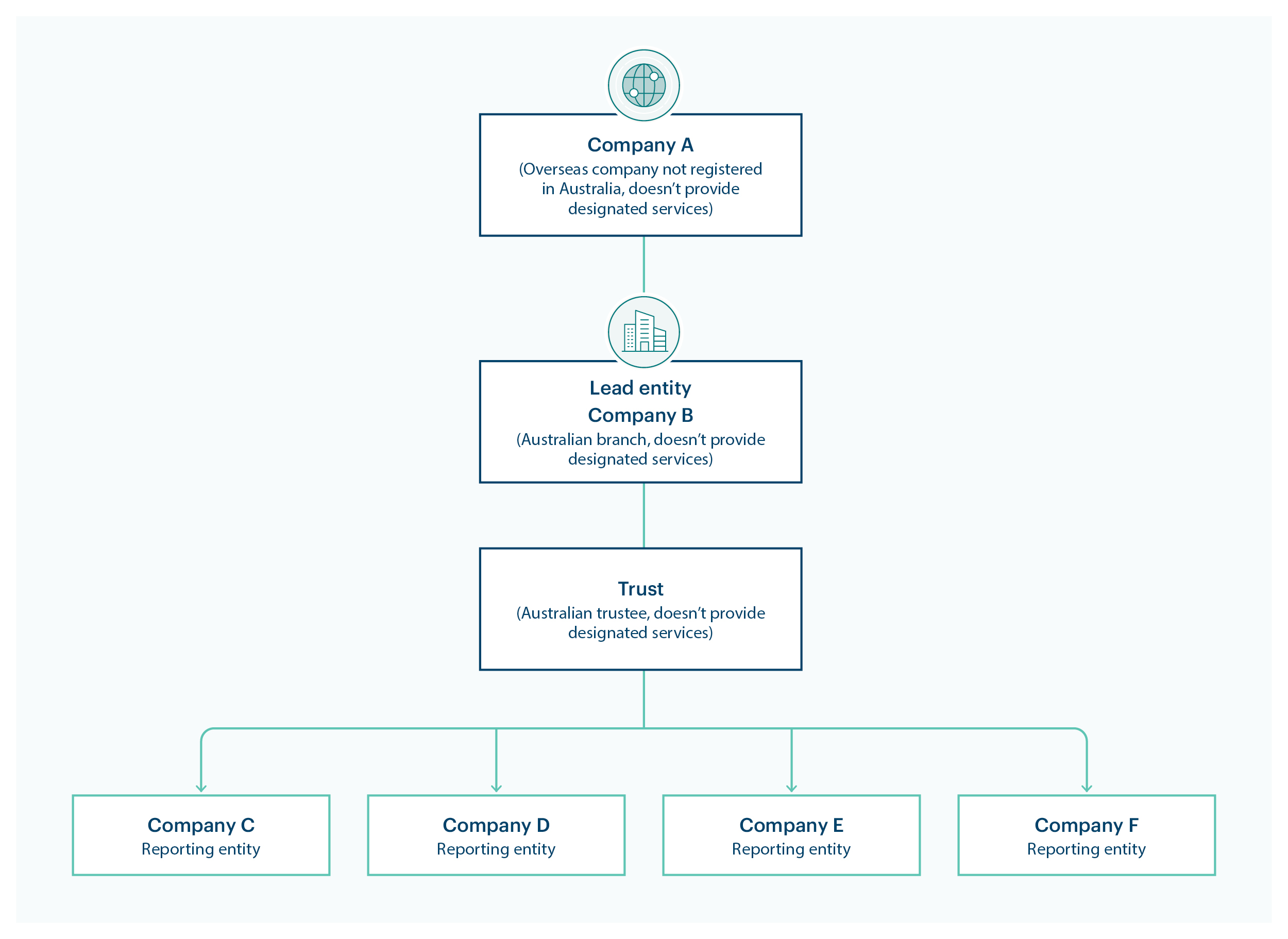

Example: Business group with foreign ownership

This example shows a business group that’s a reporting group with both an:

- overseas parent company at the top of the control structure (Company A)

- Australian based entity as the lead entity (Company B).

Company A:

- is incorporated in a foreign jurisdiction and hasn’t registered in Australia (within the meaning of the Corporations Act 2001).

- has an Australian subsidiary, Company B (Australian branch) and controls all members of the group.

Company B is an Australian incorporated person and controls a trust and appoints an Australian trustee. The trust serves no other purpose than holding 4 companies which are all reporting entities.

No reporting entity in the business group opts out of forming the reporting group.

Company A hasn’t registered in Australia so can’t be a lead entity but will still form a part of the reporting group. This means it may:

- be involved in information sharing under the group AML/CTF program

- discharge AML/CTF obligations on behalf of reporting entity members.

All members besides Company A are eligible members. This means they can all take part in deciding who the lead entity will be.

In this scenario:

- both Company B and the trust are the only two members who have the authority and capability to develop and maintain the AML/CTF policies for the group

- the eligible members can’t agree on the lead entity and still want to form a reporting group.

Because Company A has control of all other members in the group, they can appoint a lead entity who has authority and capability.

Company A appoints Company B in writing as the lead entity for the reporting group to form.

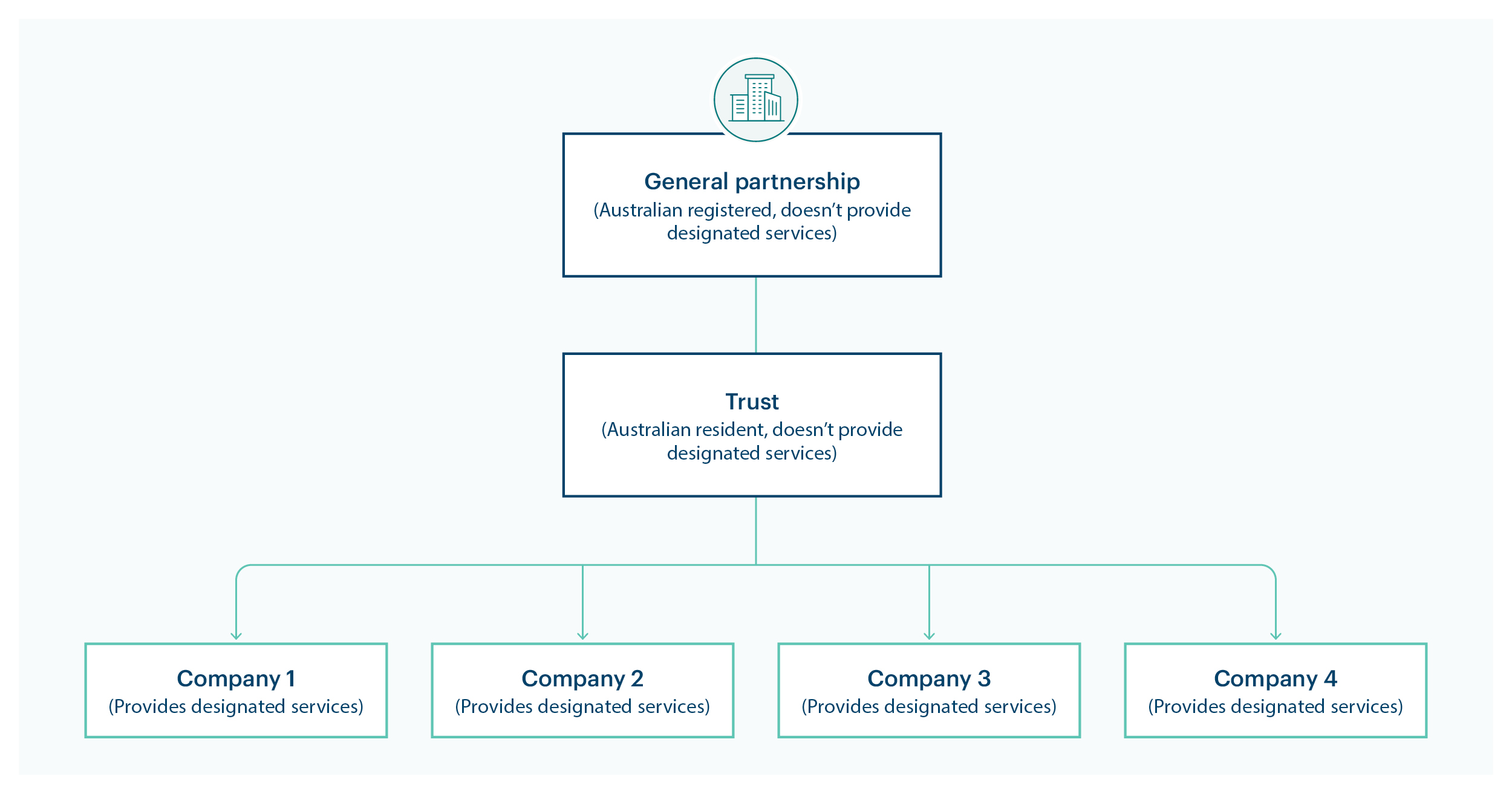

Example: A business group that can form a reporting group

This example shows the control structure of a general partnership and subsidiaries who meet the requirements of a business group.

This group can form a reporting group because:

- the general partnership controls all other persons in the group and doesn’t provide designated services

- the trust controls all companies in the group and doesn’t provide designated services

- only the general partnership and trust have the authority and capability to develop and maintain the AML/CTF policies for the group. This means that only they meet the requirement to be a lead entity.

- companies 1, 2, 3, and 4 don’t opt out of forming the reporting group

- companies 1,2,3 and 4 are reporting entities

- all members of the business group are eligible members. This is because they are Australian-based members with no member controlled by another reporting entity

- each eligible member agrees in writing on a capable lead entity – the general partnership.

Operating without a lead entity

This section refers to the Rules section 2–1(3) (a–b).

Your reporting group must not operate without a lead entity for more than 28 days.

This might happen for example, if a lead entity is acquired by a reporting entity. This means that they’re no longer eligible to be a lead entity because they’re controlled by another reporting entity.

Until a lead entity is in place, reporting entity members must either:

- continue to follow the AML/CTF policies of the previous lead entity (if there was one). This includes following their own policy if this was delegated to them by the previous lead entity.

- comply with their own individual AML/CTF policies (for new reporting groups).

If members can’t agree on a lead entity, your reporting group will cease to exist after 28 days.

Elective reporting groups

This section refers to the Rules section 2–2(3)(a–d).

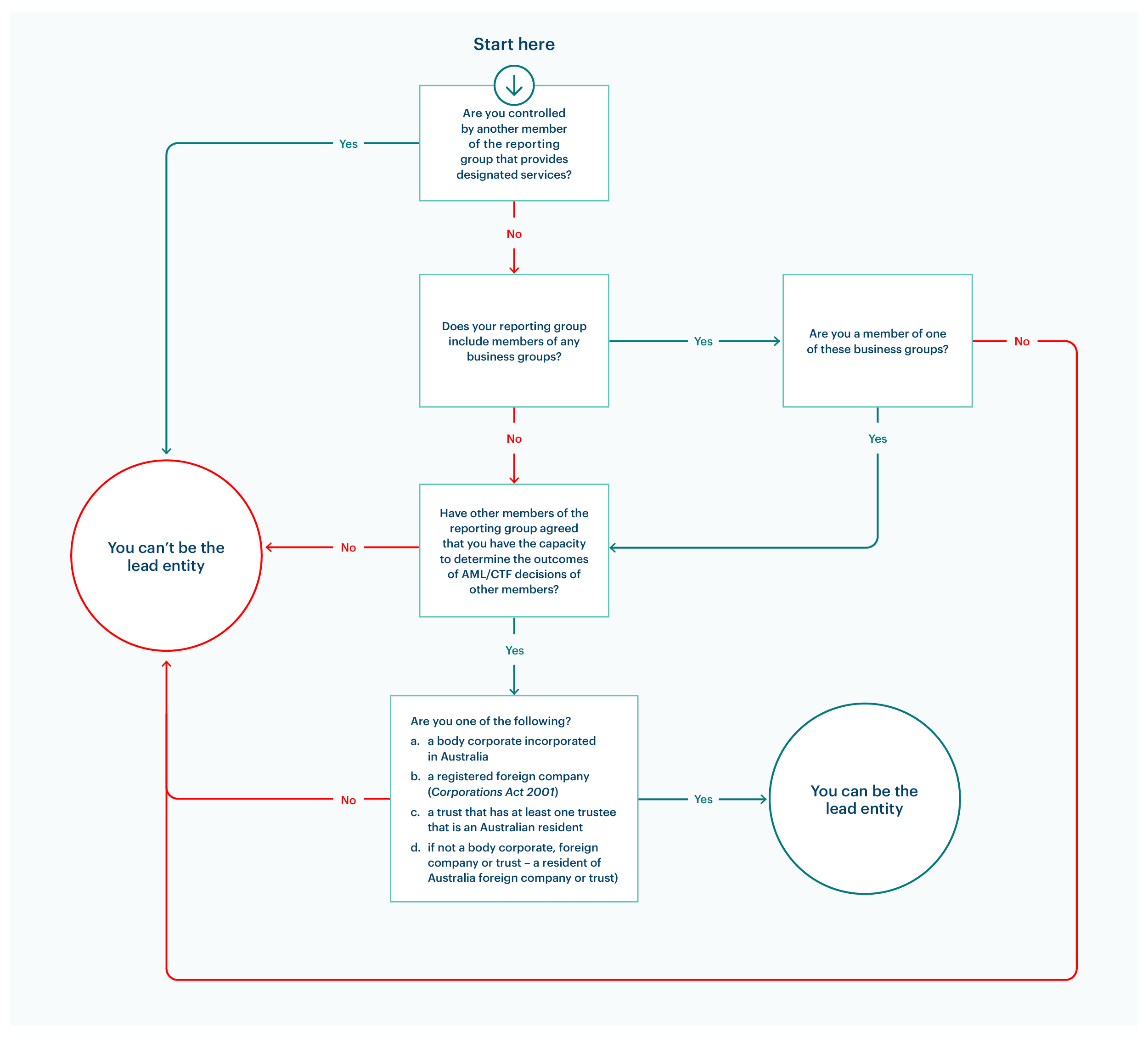

If you’re forming an elective reporting group, each one of your members must agree on a lead entity. This includes the lead entity.

Your lead entity must have the capacity to determine the outcome of the decisions about the policies of other members. Your lead entity must be a person that meets the criteria below.

If you have members from one or more business groups, your lead entity must be from one of those groups.

How to determine the lead entity of an elective reporting group

The below flowchart will help you determine who can be the lead entity in your elective reporting group.

Your elective group can’t be without a lead entity. If your answers lead you to ‘the member can’t be the lead entity’, you must restart the process.

Can I be a lead entity?

Example: Forming an elective group

A real estate franchisor and their franchisees decide to come together to form an elective reporting group. This is because the franchise agreement between them doesn’t give the franchisor control over their franchisees.

The franchisor is an Australian body corporate with subsidiaries that aren’t reporting entities. The franchisor’s subsidiaries agree to join the elective reporting group.

The franchisor agrees to act as the lead entity of the group to help the franchisees with their AML/CTF obligations.

Each member in the group agrees in writing to form a reporting group. The group consists of:

- persons who aren’t members of any other elective group

- reporting entities

- non-reporting entities, that discharge obligations on behalf of reporting entities in the group.

All members:

- agree that the franchisor has the capacity to determine the outcome of their decisions about AML/CTF policies

- will be the lead entity

- elect the franchisor as lead entity within 28 days of forming the elective group.

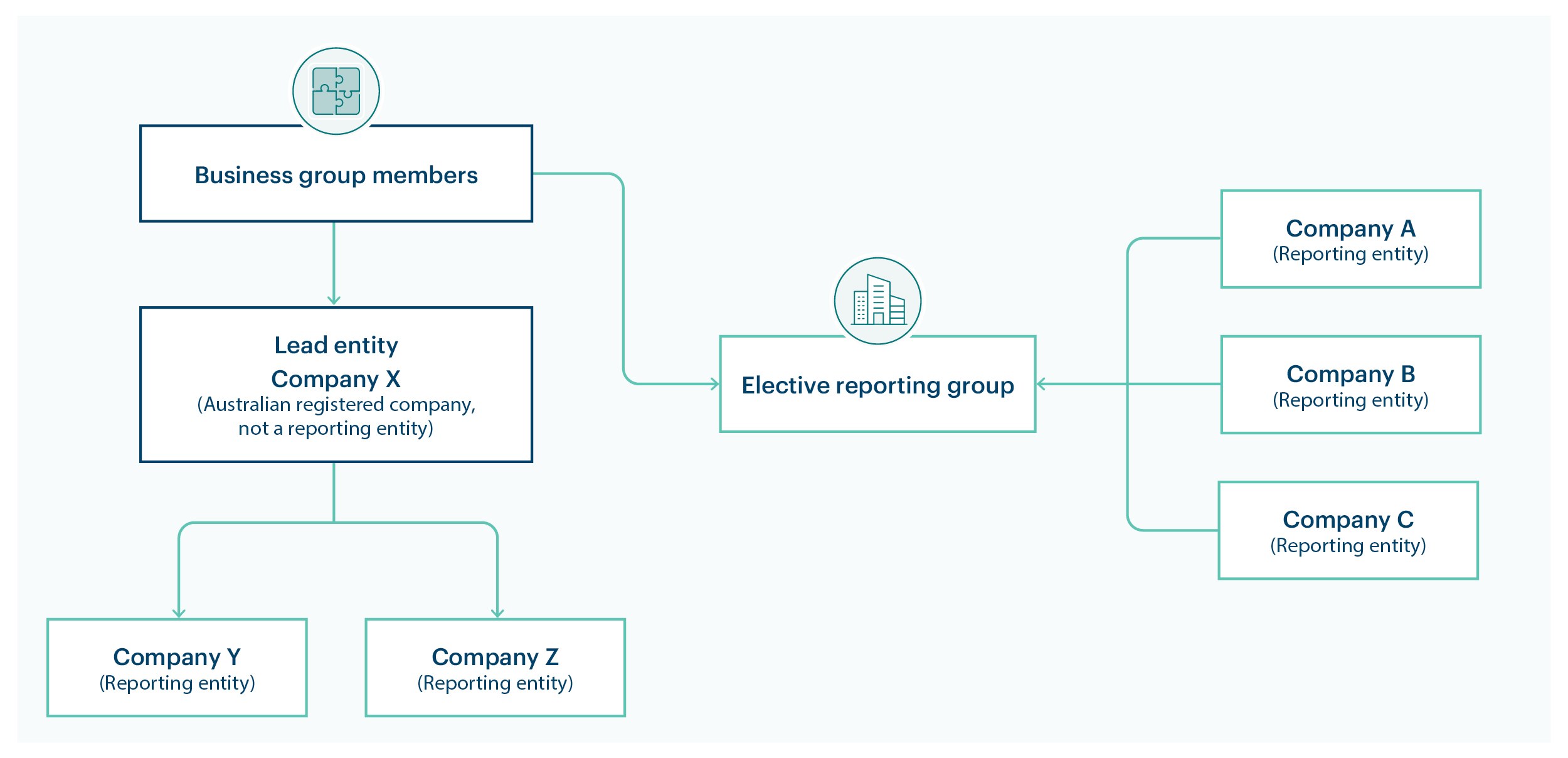

Example: Forming an elective reporting group with business group members

This example shows a scenario of a business group joining an elective reporting group with members outside its control structure:

- Company X, Y and Z are a part of the business group

- Company X controls Company Y and Z who are reporting entities

- Company X is an Australian-based member

- Company X elects in writing on behalf of Company Y and Z to form an elective group with Companies A, B and C

- Company Y and Z both agree.

Because this elective group has members of a business group within it, one of these business group members must be the lead entity.

All members (including Company X) agree in writing that Company X:

- will be the lead entity

- has the capacity to determine the outcome of decisions about the AML/CTF policies of the other members.

The elective group forms with members of a business group within it; Company A, B and C can’t be a lead entity. Company Y and Z also are not able to be a lead entity, as they do not have the capacity to determine the outcome of decisions about the AML/CTF policies of one another.

Lead entities leaving the reporting group

This section refers to the Rules sections 2–2(8) and (10)(a–b).

If you’re the lead entity of your elective reporting group, and want to leave the group, you can elect to do so. However, you must give each member of the group written notice.

The elective group must not operate without a lead entity for more than 28 days. Each member in your reporting group must agree on a new lead entity within this time.

The elective group must continue to comply with the AML/CTF policies of the previous lead entity.

Related pages

This guidance sets out how we interpret certain Australian legislation, along with associated Rules and regulations. Australian courts are ultimately responsible for interpreting these laws and determining if any provisions of these laws are contravened.

The examples and scenarios in this guidance are meant to help explain our interpretation of these laws. They’re not exhaustive or meant to cover every possible scenario.

This guidance provides general information and isn't a substitute for legal advice. This guidance avoids legal language wherever possible and it might include generalisations about the application of the law. Some provisions of the law referred to have exceptions or important qualifications. In most cases your particular circumstances must be taken into account when determining how the law applies to you.