Learn about correspondent banking relationships, and what you must do when entering or continuing a correspondent banking relationship that will involve a vostro account.

Correspondent banking relationship definition

This section refers to section 5 of the Act

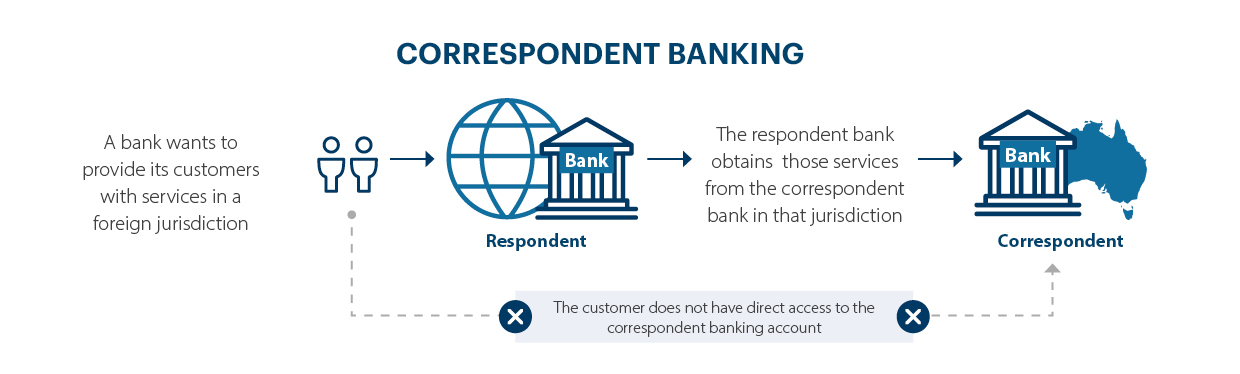

A correspondent banking relationship involves a financial institution (the correspondent) providing banking services to another financial institution (the respondent) located in another country.

The respondent may be a subsidiary or related company of the correspondent. The concepts of related company and subsidiary are described in sections 46 and 50 of the Corporations Act 2001.

Correspondent banking relationships enable the respondent to provide its own customers with cross-border products and banking services that it can’t provide itself, typically in a jurisdiction that the respondent doesn’t have a presence in.

Due to the high money laundering, terrorism financing and proliferation financing risks (we refer to these as ML/TF risks) of these relationships, appropriate due diligence of the relationship is essential to make sure you comply with your obligations under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (the Act).

Services can include providing a current or other liability account and related services such as:

- cash management

- international funds transfers

- cheque clearing

- trade finance arrangements

- foreign exchange services

- providing customers of the respondent with direct access to accounts with the correspondent (and vice versa).

The scope of a relationship and extent of products and services supplied depend on the needs of the respondent, and the correspondent’s ability and willingness to supply them.

In the context of a correspondent banking relationship, the correspondent broadly acts on behalf of or as an intermediary for the respondent and executes and processes payments or other transactions for customers of the respondent.

The underlying customers of the respondent financial institution may be:

- individuals

- non-individuals like bodies corporate

- other financial services firms.

Types of correspondent banking relationships

Correspondent banking relationships may be used in various ways. You should be aware of and assess the ML/TF risks arising from these arrangements.

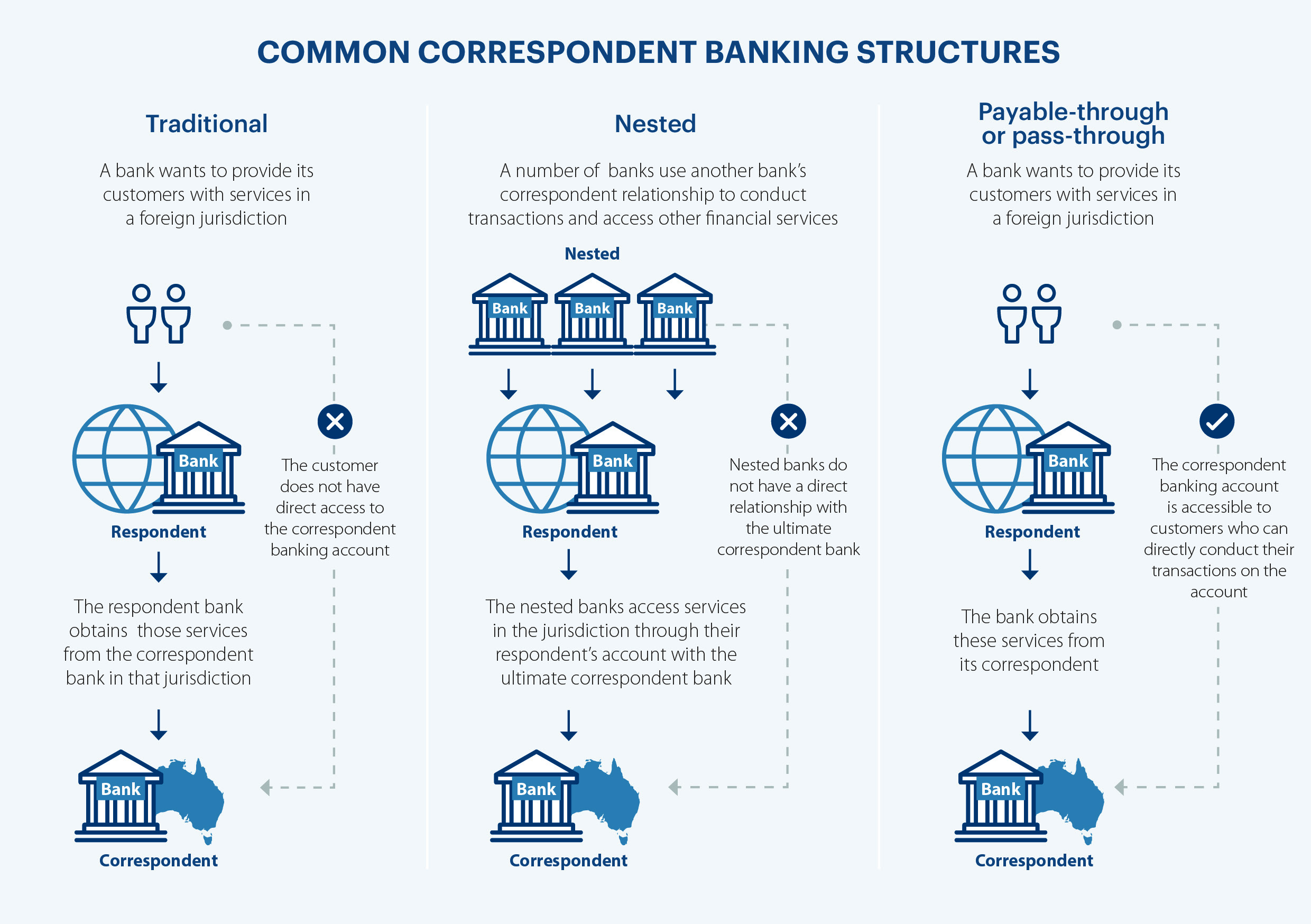

Traditional correspondent banking

In this type of arrangement, a correspondent financial institution opens and maintains an account for a respondent financial institution and handles payments. This allows the respondent to provide equivalent services to its own customers. However, the customers of the respondent don’t have direct access to the correspondent banking account.

Downstream correspondent clearance

Downstream correspondent clearance (or nesting) involves a number of indirect respondent financial institutions using a direct respondent financial institution’s correspondent relationship to conduct transactions and obtain access to other financial services from the correspondent.

Indirect respondent financial institutions don’t have the direct relationship with the correspondent and they indirectly access financial services in the target jurisdiction through their direct respondent’s account with the ultimate correspondent.

The indirect respondent financial institutions conduct transactions and obtain access to other financial services without being direct customers of the correspondent.

This is different from traditional correspondent banking because there is an additional financial institution (the respondent) mediating between the indirect respondent financial institutions and the correspondent financial institution. While an Australian correspondent financial institution isn’t required to conduct due diligence assessments on indirect respondents, you must assess the higher ML/TF risks associated with these types of arrangements.

Payable-through or pass-through accounts

In this type of arrangement, the account that the respondent financial institution holds with the correspondent financial institution is accessible to its customers. Customers can directly conduct their transactions in this account by making deposits and writing cheques on the account.

Source: Closing the loop: AML/CFT supervision of correspondent banking, Rodrigo Coelho, Jonathan Fishman, Amer Hassan and Rastko Vrbaski, Bank for International Settlements, September 2020.

Vostro accounts

A vostro (Latin for ‘yours’) account is an account provided by the correspondent financial institution to be held by a respondent financial institution under a correspondent banking relationship.

You should understand this term to have its ordinary meaning, including by reference to the Wolfsberg Anti-Money Laundering Principles for Correspondent Banking.

Even if an account isn’t described as a ‘vostro account’ by the correspondent or respondent institution, if it fulfils such a purpose in practice it’s a vostro account. In determining if an account is a vostro account, we caution financial institutions against taking an overly narrow or technical approach.

A nostro (Latin for ‘ours’) account refers to an account that a financial institution holds in a foreign currency in another financial institution.

The requirement to conduct due diligence assessments under Part 8 of the Act is triggered by the provision of a vostro account. The due diligence assessment is focused on ensuring that you understand the:

- ownership and control of the respondent institution

- anti-money laundering and counter-terrorism financing (AML/CTF) context in which it operates

- effectiveness of its AML/CTF policies, procedures, systems and controls (we refer to these as AML/CTF policies).

Extra due diligence for correspondent banking relationships that will involve a vostro account

Correspondent banking relationships are recognised globally as being vulnerable to exploitation for ML/TF.

A correspondent typically has limited information about the respondent financial institution’s customers and the nature of their transactions. They rely on their understanding of the respondent’s AML/CTF policies to satisfy themselves of the levels of ML/TF risk. This can expose the correspondent financial institution to weaknesses in the respondent’s AML/CTF risk policies, increasing the associated risks.

The correspondent often has no direct relationship with the underlying parties to a transaction and doesn’t carry out customer due diligence (CDD) on the respondent’s customers. Correspondents often have limited information about the nature or purpose of the underlying transactions, particularly when processing electronic payments.

The ML/TF risks and vulnerabilities may be higher where the respondent is located in a foreign country assessed under the Financial Action Task Force’s (FATF) Mutual Evaluation processes as having weak AML/CTF laws, or poor or limited supervision of those laws.

Correspondent banking relationships, if poorly managed, can allow other financial institutions with inadequate AML/CTF policies, and customers of those institutions, direct access to international banking systems.

For any correspondent, the highest risk correspondent banking relationships involve providing a vostro account to respondents that are any of the following:

- offshore financial institutions that are limited to conducting business with non-residents or in another non-local currency, and aren’t subject to appropriate supervision of their AML/CTF policies

- offer downstream correspondent clearing services (or nesting)

- are domiciled in jurisdictions with weak regulatory frameworks or other significant risk factors such as corruption.

Correspondent banking due diligence and other AML/CTF obligations

Correspondent banking due diligence complements other AML/CTF obligations like CDD.

For example, opening a vostro account involves providing designated service Item 1 of Table 1 in subsection 6(2) of the Act (opening an account as an ADI). Providing other services under a correspondent banking relationship may constitute other designated services.

For these services, you must comply with other AML/CTF obligations in respect of the respondent and its beneficial owners (if any), such as initial and ongoing customer due diligence, and submitting reports to us when required.

Exemption

Under section 39E of the Act a correspondent financial institution is exempt from conducting initial customer due dligence on a customer if the designated service meets all of the following:

- it’s covered by Item 2 or 3 of Table 1

- relates to a correspondent banking relationship

- has a geographical link in accordance with section 100 of the Act

- relates to signatories to the account who are employees of the other financial institution.

Downstream correspondent clearance

When these services are offered to a respondent that’s itself a downstream correspondent clearer, we expect you to:

- use a risk-based approach

- take into account the types of financial institutions to whom the respondent offers such services when identifying and assessing the ML/TF risk you face in providing related designated services

- consider the degree to which the respondent examines the AML/CTF controls of those financial institutions.

You must also implement AML/CTF policies to ensure the respondent doesn’t have its own correspondent banking relationships with shell banks, or allow its accounts to be used by shell banks.

Refer to the Wolfsberg Correspondent Banking Due Diligence Questionnaire (February 2018).

Prohibition on entering a correspondent banking relationship with a shell bank

This refers to sections 94A and 95 of the Act

You must not enter into correspondent banking relationships with any of the following:

- shell banks

- financial institutions that have correspondent banking relationships with shell banks

- financial institutions that allow their accounts to be used by shell banks.

When you must terminate a correspondent banking relationship

You must terminate a correspondent banking relationship within 20 days (unless our CEO allows a longer period) of becoming aware that the respondent is any of the following:

- a shell bank

- has a correspondent banking relationship with a shell bank

- permits its accounts to be used by a shell bank.

If the respondent permits its accounts to be used by a shell bank, you may ask the respondent to terminate its correspondent banking relationship with the shell bank rather than terminating your correspondent banking relationship with the respondent.

If the respondent hasn’t complied with the request to terminate the relationship 20 business days after you made the request, you must terminate your relationship with the respondent within a further 20 days (unless our CEO allows a longer period).

This is an absolute prohibition against any form of correspondent banking relationship. It’s not limited to the provision of a vostro account.

For example, holding a nostro account with a shell bank is prohibited, regardless of whether the shell bank holds a vostro account.

Geographical links

This section refers to section 100 of the Act

You can only be subject to the correspondent banking provisions of the Act if you do any of the following:

- carry on an activity or business at or through a permanent establishment in Australia (for example, an entity situated in Australia or an Australian branch of an overseas entity)

- are a resident of Australia and carry on an activity or business at or through a permanent establishment in a foreign country (for example, a foreign branch of an Australian entity)

- are a subsidiary of a company that’s a resident of Australia and the financial institution carries on an activity or business at or through a permanent establishment in a foreign country (for example, an overseas subsidiary of an Australian entity).

Permanent establishment is defined in section 21 of the Act, and includes provision for agents, mobile services and electronic communications.

What you must do before entering into correspondent banking relationships

This section refers to section 96 of the Act and section 7-1 of the Rules.

Before entering a correspondent banking relationship that will involve a vostro account you must:

- carry out a due diligence assessment in accordance with section 7-1 of the Anti-Money Laundering and Counter-Terrorism Financing Rules (the Rules

- prepare a written record of that assessment

- obtain the approval of a senior officer within your financial institution.

Learn more about each of these requirements below.

When a financial institution ‘enters into’ a correspondent banking relationship

We consider that a financial institution enters into a correspondent banking relationship at the earlier of:

- the agreement establishing the relationship coming into effect, regardless of whether that is by a legally binding arrangement or some other arrangement

- opening of a vostro account by one of the parties.

What you must consider as part of your due diligence assessment

You must consider the factors listed below in your due diligence assessment before you enter into a correspondent banking relationship that will involve a vostro account.

You must also consider these factors when you conduct ongoing due diligence assessments.

Ownership, control and management structures

You must consider the ownership, control and management structures of the respondent financial institution and its ultimate parent (if any). For example:

- if publicly owned, whether its shares are traded on a recognised market or exchange in a jurisdiction with a satisfactory regulatory regime

- if privately owned, the identity of any beneficial owners and controllers

- the location, structure and experience of the board of directors and executive management including if any key personnel are politically exposed persons (PEPs)

- relevant information from the respondent’s website and latest annual return.

Nature, size and complexity of the respondent’s business

You must consider the nature, size and complexity of the respondent’s business, including the:

- products and services offered

- delivery channels it uses to provide services

- kinds of customers it has.

You must also consider both the:

- kinds of transactions that would be carried out on behalf of underlying customers as part of the correspondent banking relationship

- services that would be provided to underlying customers that relate to such transactions.

The type of business the respondent engages in and the type of markets it serves, will help you assess the ML/TF risk the respondent presents.

Foreign countries

You must consider the foreign countries in which the respondent operates or is a resident.

If the ultimate parent company of the respondent has group-wide AML/CTF systems and controls that the respondent operates within, you must consider the country or countries the ultimate parent operates in or is a resident of.

In relation to any foreign country or countries identified, you must consider both the:

- existence and quality of any AML/CTF regulation and supervision in those countries

- respondent’s compliance practices in relation to those regulations.

For example, consider the quality of supervision by the primary AML/CTF regulatory body responsible for overseeing or supervising the respondent.

AML/CTF regulations and supervision

You must assess the appropriateness of the respondent’s AML/CTF policies, procedures, systems and controls.

Consider whether the respondent is regulated for AML/CTF and, if so, whether the respondent is required to verify the identity of its customers and apply other AML/CTF controls to FATF or equivalent standards.

if you are undertaking due diligence on a branch, subsidiary or affiliate, consideration may be given to the parent having robust group-wide controls, and whether the parent is regulated for AML/CTF to FATF or equivalent standards.

You may also wish to use established industry questionnaires (for example, the Wolfsberg Correspondent Banking Due Diligence Questionnaire or similar tools to meet this requirement. Additionally, you may also wish to speak with representatives of the respondent to determine if senior management recognise the importance of AML/CTF controls.

Publicly available information and reputation

You must consider publicly available information about the reputation of:

- the respondent

- any members of the business group that the respondent is a member of, that are a remitter, virtual asset service provider or financial institution.

This includes whether the respondent or any of those members has been the subject of:

- a regulatory investigation relating to its implementation of AML/CTF or sanctions obligations

- adverse regulatory action relating to implementation of AML/CTF or sanctions obligations

- an investigation or criminal or civil proceedings relating to money laundering, terrorism financing or other serious crimes.

Payable-through accounts

If you’ll provide a vostro account that can be directly accessed by the customers of the respondent (payable-through accounts), you must consider whether the respondent will both:

- undertake initial CDD and ongoing CDD on those customers

- be able to provide, on request, information collected when conducting initial and ongoing CDD, and the reliable and independent data used to verify the information.

Note: If the respondent is unable to provide this data and documentation, then you must not provide a payable-through-account.

Senior officer approval

This section refers to section 96 of the Act and section 7-2 of the Rules

A senior officer of your financial institution must give approval before you enter into a correspondent banking relationship.

For the purposes of correspondent banking relationships, a senior officer doesn’t have to be a person in executive management. You can determine who is a senior officer, depending on the size and complexity of your organisation.

We expect your senior officer to have sufficient knowledge of your ML/TF and serious crime risk exposure, and sufficient authority to make decisions affecting your risk exposure.

Considerations for senior officer approval

When deciding to approve entering into a correspondent banking relationship, the senior officer must consider both the:

- risks of ML/TF and other serious crimes assessed in the written record of your due diligence assessment in relation to entering the correspondent banking relationship

- appropriateness of your AML/CTF program to manage and mitigate those risks.

If you’re to maintain payable-through accounts, the senior officer must also consider if they’re satisfied that the respondent:

- will undertake initial and ongoing CDD for customers that have access to the payable‑through accounts

- would be able to provide you, on request, with information collected when the respondent undertakes that initial and ongoing CDD and the reliable and independent data used to verify the information.

Documentation of responsibilities under correspondent banking relationships

If you enter into a correspondent banking relationship with another financial institution that involves a vostro account, you must prepare a written record within 20 business days after the day of entering into the relationship that sets out both:

- your responsibilities under that relationship

- the responsibilities of the other financial institution under that relationship.

This includes any other AML/CTF-related expectations you have concerning your respondent institutions. What these expectations are will depend on your circumstances, including the size, nature and complexity of your respondent’s business, and the results of your due diligence assessments.

Ongoing due diligence of correspondent banking relationships

This section refers to section 96 of the Act and sections 7-3 and 7-4 of the Rules.

You must conduct ongoing due diligence in relation to your correspondent banking relationships involving a vostro account. You must conduct these assessments at times you determine are appropriate based on:

- the level of ML/TF and other serious crime risk

- any material changes in those risks.

At a minimum, you must carry out a due diligence assessment at least every 2 years.

You must also conduct a due diligence assessment and review the correspondent banking relationship if either:

- your respondent has been subject to an investigation or regulatory action, which leads to a material change in the ML/TF or serious crime risk

- there has been any other material change that impacts on the ML/TF or serious crime risk associated with the relationship.

We expect your policies, systems, controls and procedures relating to your correspondent banking relationship to be reviewed and updated in line with your AML/CTF policies.

What you must consider when carrying out ongoing due diligence assessments

Your ongoing due diligence assessments must consider the same factors that are required for due diligence assessments before entering a correspondent banking relationship.

Additionally, you must also consider and address any material changes to those risks (for example, changes in the respondent financial institution’s business model) or to your business relationship with the respondent, including the types of transactions carried out as part of the relationship.

You should be satisfied that the respondent continues to have in place and maintain appropriate risk-based systems and controls to mitigate and manage ML/TF and serious crime risks.

Other factors to consider include, but aren’t limited to:

- changes in behaviour or activity, for example, sudden or significant changes in transaction activity by value or volume, or unusual transactions

- you should conduct transaction monitoring on the respondent institution and the associated underlying transactions

- significant increases of activity or consistently high levels of activity with higher risk countries or regions or higher risk entities

- activity that may, in the absence of other explanation, indicate possible money laundering, such as the structuring of transactions under reporting thresholds

- material changes in ownership or management structure

- re-classification of the country or region where the respondent institution is located

- identification of relationships with politically exposed persons (PEPs), either as customers or through involvement in the ownership and control structures

- adverse media coverage of the respondent institution.

Recording your assessments of the correspondent banking relationship

You must prepare a written record on completion of each ongoing due diligence assessment of your correspondent banking relationships within 10 business days of completing the assessment.

Initial and ongoing due diligence assessments

When conducting initial and ongoing due diligence assessments, consider both the direct use accounts and other exchange relationships or other types of accounts that can be transacted through.

Examples to consider include:

- accounts posing a high ML/TF risk

- the expected activity through each account

- deposit accounts (or equivalent) held by higher-risk financial institutions

- accounts used to provide services to third parties, for example, cash management trusts

- accounts held for foreign embassies or consulates, which may pose higher risks (for example, personal transactions through an embassy account)

- downstream correspondent clearance, when a foreign financial institution accesses the Australian financial system in effect anonymously, by operating through the correspondent banking account belonging to another foreign financial institution

- payable-through accounts, requiring your to being satisfied that the other financial institution has verified the identity of and performed ongoing due diligence on customers that have direct access to accounts of the other financial institution and is able to provide relevant customer identification information upon request.

Related pages

Additional resources

The following resources may help when developing due diligence processes for correspondent banking relationships.

- Wolfsberg Banking Anti Money Laundering Correspondent Banking Principles

- Wolfsberg Correspondent Banking Due Diligence Questionnaire

- Financial Action Task Force (FATF)(external link) including Mutual Evaluation Reports, guidance and other key publications such as high risk and monitored jurisdictions.

- The Egmont Group

- Organisation for Economic Co-operation and Development (OECD)

- The World Bank

- International Monetary Fund (IMF)

- Bank Secrecy Act/Anti-Money Laundering Examination Manual

- Joint Money Laundering Steering Group (JMLSG) Guidance Notes

- The Clearing House Association LLC Guiding Principles for Anti-Money Laundering Policies and Procedures in Correspondent Banking

This guidance sets out how we interpret certain Australian legislation, along with associated Rules and regulations. Australian courts are ultimately responsible for interpreting these laws and determining if any provisions of these laws are contravened.

The examples and scenarios in this guidance are meant to help explain our interpretation of these laws. They’re not exhaustive or meant to cover every possible scenario.

This guidance provides general information and isn't a substitute for legal advice. This guidance avoids legal language wherever possible and it might include generalisations about the application of the law. Some provisions of the law referred to have exceptions or important qualifications. In most cases your particular circumstances must be taken into account when determining how the law applies to you.