Learn about how to determine ownership and control.

Learn about ownership and control to help you identify:

- who the beneficial owners of your customers are for initial customer due diligence

- if you’re in a business group

- who the lead entity of your business or elective reporting group could be

- if you satisfy the geographical link test.

Terms we use on this page

Where we use the word person throughout this guidance, this includes any of the following:

- an individual

- a company

- a trust

- a partnership

- a corporation sole

- a body politic (including a government body)

- an unincorporated association.

The term customer in this guidance refers to customers who are a person (as referred to above) other than an individual.

Beneficial ownership

This section refers to the Act section 5.

A beneficial owner of a customer means an individual who directly or indirectly does any of the following:

- owns 25% or more of the customer

- controls the customer.

Ownership can be either:

- direct, such as through shareholding

- indirect, such as through another company’s ownership structure, or through an intermediary like a bank or broker.

When determining this beneficial ownership, there may be a chain of owners. This could include other persons who control or own 25% or more of your customer. You must follow this chain of ownership until you can determine the individual(s) who are the beneficial owner(s) of the customer.

Control

This section refers to the Act section 11.

Control refers to a person’s ability to influence or direct the decision-making process of another person. Control can be either:

- formal and direct, through ownership and voting rights

- through practical influence and established patterns of behaviour.

You don’t need to own another person to have control.

Control of a body corporate

This section refers to the Act section 11(1)(a-d).

A person ‘controls’ a body corporate (such as a company) if any of the following apply:

- Voting power – the person has the capacity to cast, or control the casting of, more than 50% of votes at a general meeting.

- Shareholding – the person directly or indirectly holds more than 50% of issued share capital (excluding shares that carry no right to participate beyond distribution of profits or capital, or mutual capital instruments).

- Board control – the person can control the composition of the board or governing body.

- Practical influence – the person can determine the outcome of decisions about financial and operational policies, considering any practical influence (rather than rights to be enforced) and practice or pattern of behaviour that affects those policies.

Control of a person other than a body corporate

This section refers to the Act section 11(2)(a-b).

Assessing the control of a person who isn’t a company (such as a partnership, trust or individual) is based on:

- Board control – the person can control the composition of any governing body (such as trustees, managers and committee).

- Practical influence – the person can determine the outcome of decisions about financial and operational policies, considering any practical influence (rather than rights to be enforced) and pattern of behaviour.

Determining ownership and control

This section refers to the Act section 28.

Customers may have complex ownership structures, and their beneficial owners can be difficult to identify. You must know how your customer is owned, controlled and managed.

Usually, you can ask the customer for the information you need. However, you may need to do your own research.

Documents that can help you with your research include:

- information on ASIC registers

- annual statements including the amendments submitted to ASIC

- current and historical company extracts from ASIC.

Other documents that can help include:

- the company’s constitution and/or memoranda

- trust deeds

- partnership agreements

- constitutions of registered cooperatives

- distribution statements to shareholders.

Public professional registers, such as the Financial Advisers Register, can also help. You can use these to check companies’ association with a professional, such as a financial adviser.

You may also choose to engage with third party services. These services may be able to provide you with beneficial ownership information at a cost.

Beneficial ownership examples

Read our examples of beneficial ownership.

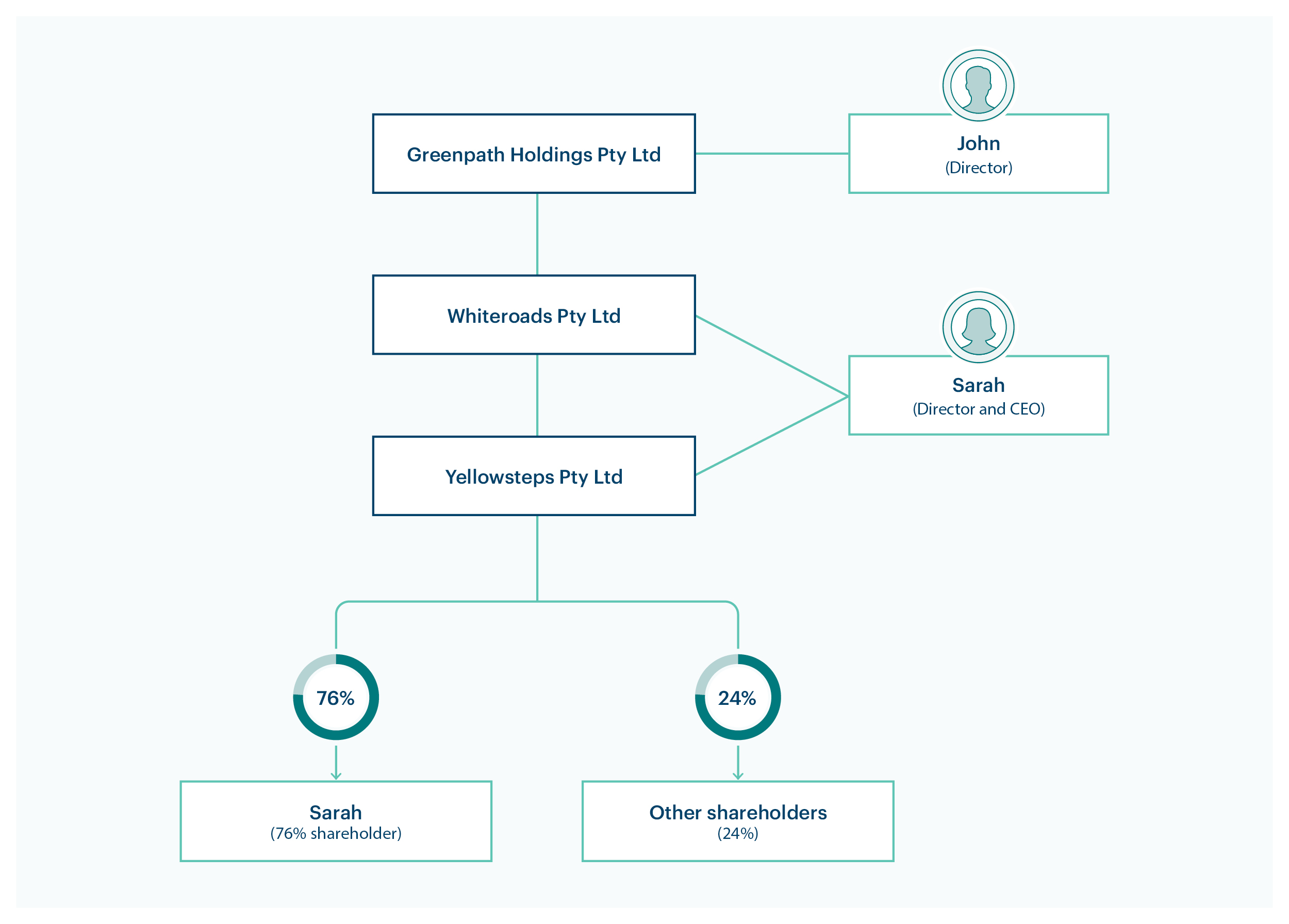

Example: determining beneficial ownership of a company

Summerset Bank is a mid-sized financial institution. John is the sole director of Greenpath Holdings Pty Ltd. He attends a branch in person to apply for a business transaction account for the company.

The bank begins initial CDD on Greenpath Holdings Pty Ltd as the customer. They identify John as the authorised agent to act on behalf of the customer as its sole director.

As part of their initial CDD process, the bank requests identification documents from John. They also request documents to show the company’s corporate and ownership structure. John submits documents with this information.

The bank begins reviewing the company documents to identify the beneficial ownership and organisational structure. They notice that Whiteroads Pty Ltd is its sole shareholder.

Summerset does a more in-depth search by getting current and historic ASIC searches of both:

- Greenpath Holdings Pty Ltd

- Whiteroads Pty Ltd.

The ASIC search identifies that a third company, Yellowsteps Pty Ltd, owns Whiteroads Pty Ltd.

Summerset does further ASIC checks and uncovers that Sarah:

- owns 76% of Yellowsteps Pty Ltd

- acts as the sole director and thus assumed to be a key decision maker of Yellowsteps Pty Ltd and Whiteroads Pty Ltd.

No other individual owns 25% or more of Yellowsteps Pty Ltd.

Summerset has established that Sarah ultimately owns Greenpath Holdings Pty Ltd. Summerset submits a request for further information from John, explaining they need to verify Sarah’s identity as well.

John gives Sarah’s phone number and Summerset asks her to provide documents to verify her identity. Sarah goes to a branch of the bank and brings her driver’s licence and a utility bill in her name.

Summerset verifies the identity information using the document verification system (DVS). They find no differences in the information Sarah provided. Summerset checks if Sarah is:

- a politically exposed person

- subject to sanctions

- linked to any high-risk jurisdiction lists.

Their search results in no matches.

Because of their findings, Summerset assigns a medium risk rating for Greenpath Pty Ltd. This is due to the legal ownership structure and is in line with their ML/TF risk assessment. They open the account.

The bank then uploads all documents to the customer file. This includes the ownership path and all 3 company extracts.

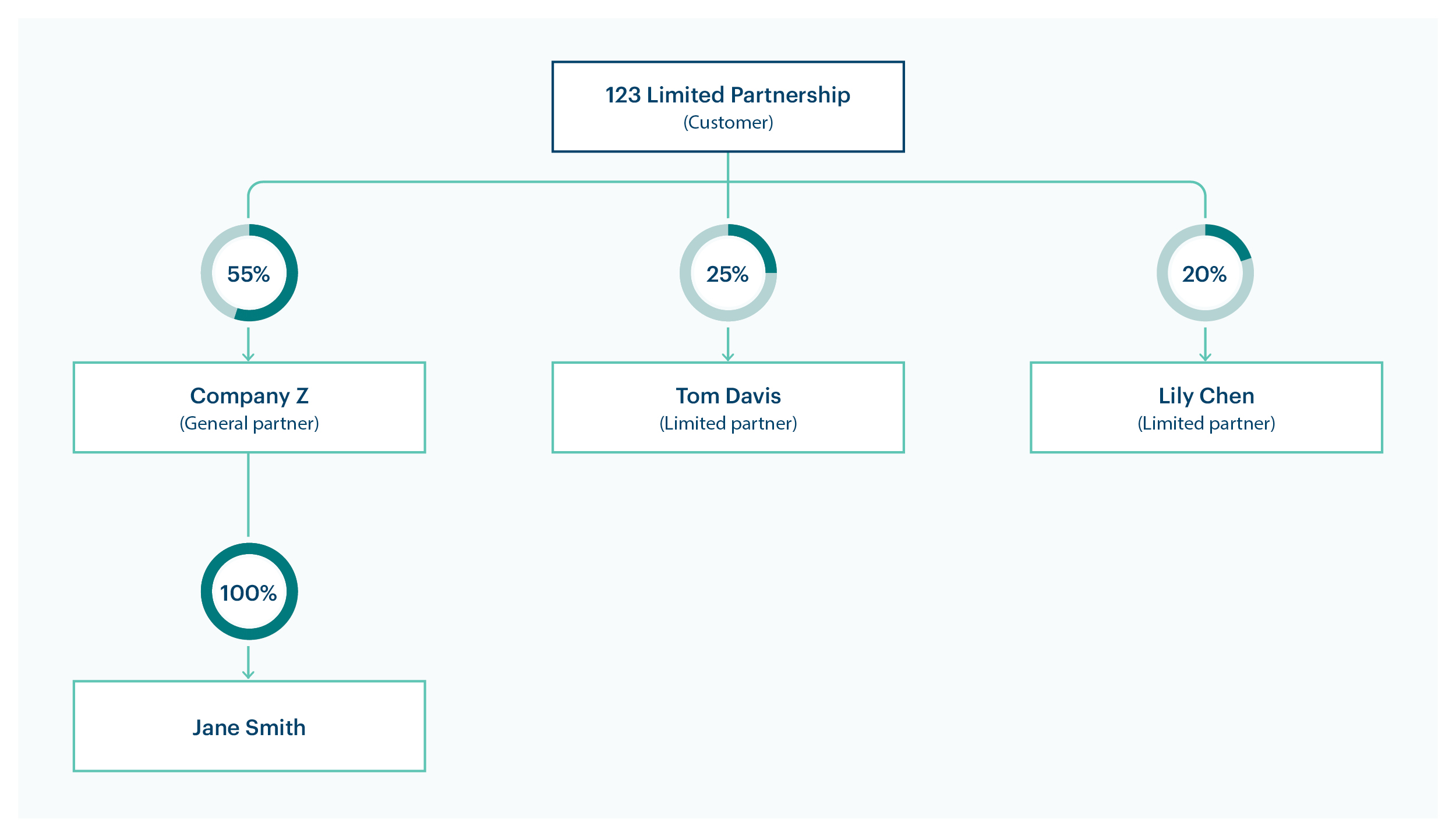

Example: determining beneficial ownership of a limited partnership

A law firm is trying to identify the beneficial owner of their prospective customer, 123 Limited Partnership. They’ve asked to view the partnership agreement.

Based on 123 Limited Partnership’s partnership agreement:

- They have one general partner (Company Z) and 2 limited partners. Tom Davis who holds 25% of the capital, Lily Chen who owns 20% of the capital and they both have profit entitlement but no voting rights.

- Company Z is the general partner. It holds 55% of the capital, profit entitlement and holds all voting rights in 123 Limited Partnership.

- Company Z isn’t acting as a nominee general partner.

- Jane Smith is the sole shareholder of Company Z.

Tom Davis is a beneficial owner based on his 25% ownership in the limited partnership.

Jane Smith is a beneficial owner based on her ownership of Company Z, which controls the limited partnership.

Reporting groups that are business groups examples

This section refers to the Act sections 10A(1)(a) and (3) and the Rules sections 2–1(1) and (2).

A business group exists when one person controls one or more persons. The members of the business group will then be all persons within the control structure.

Your business group becomes a reporting group if at least one member provides designated services.

To remain a reporting group the group must ensure that, within 28 days, either:

- all eligible members agree in writing on a lead entity

- the person who controls all other members appoints a lead entity, in writing.

An eligible member is one that is both:

- not controlled by any member of the business group that provides designated services

- a body corporate, resident or a registered foreign company in Australia or a trust with at least one trustee that is a resident in Australia.

Your lead entity can be any member of the business group that is all of the following:

- not controlled by any member of the business group that provides designated services

- is capable and is authorised, including by consent, to develop and maintain the group’s anti-money laundering and counter-terrorism financing (AML/CTF) policies

- a body corporate, resident or a registered foreign company in Australia or a trust with at least one trustee that is a resident in Australia.

Learn more about forming reporting groups.

The following examples help identify members of the reporting group and lead entities.

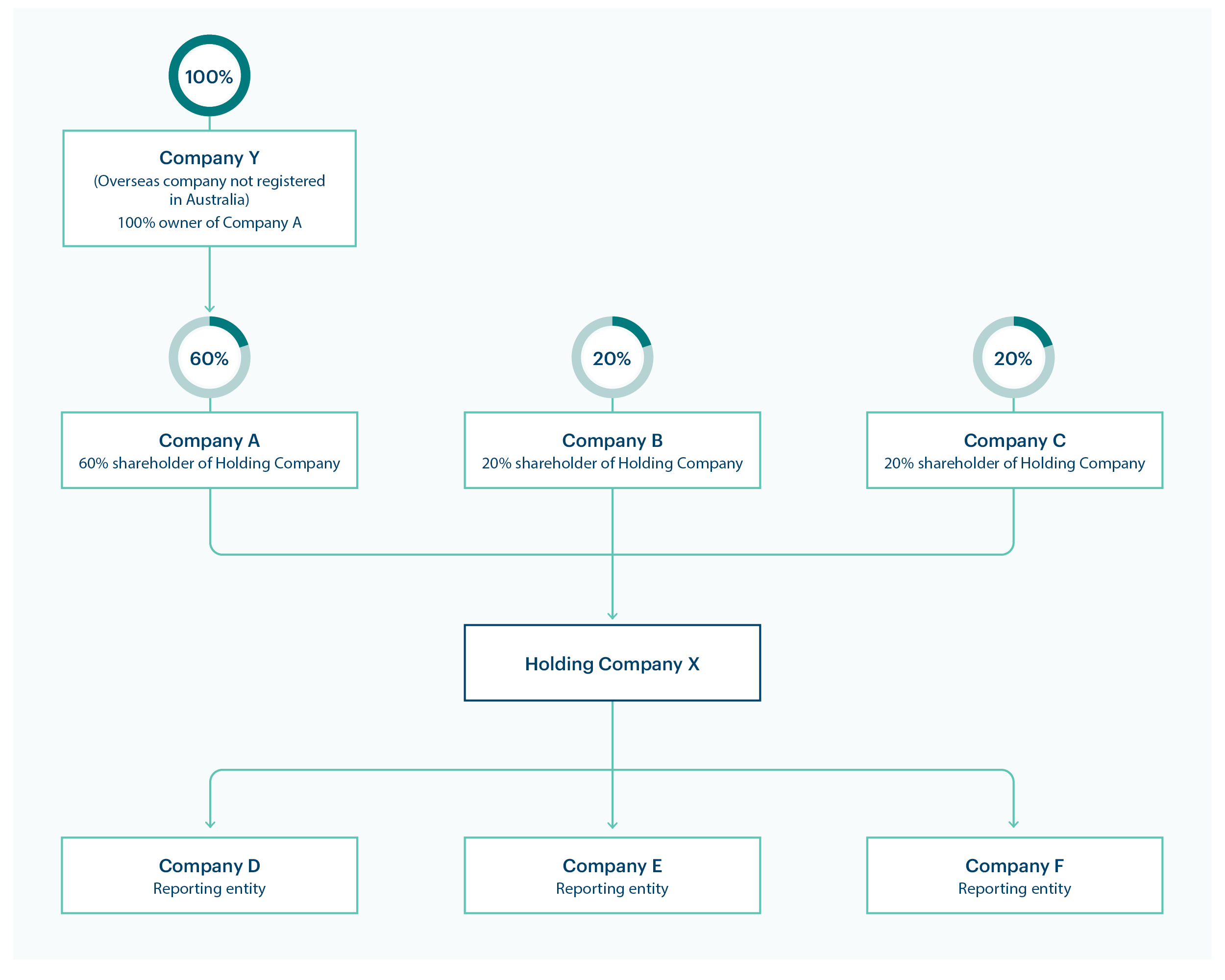

Example: shareholder control

All the companies above are incorporated in Australia except for Company Y, which is a foreign company not registered in Australia and does not provide designated services.

The 3 reporting entities (Company D, Company E and Company F) are trying to identify if they:

- are in a business group and who the members will be

- can be a reporting group, and who the lead entity could be

Who are the members of the business group

They break the business structure down in the following way:

- Company Y is the sole shareholder of Company A and controls all other members in the group.

- Company A is the majority shareholder of Holding Company X. Therefore, it controls Holding Company X and reporting entities Companies D, E and F.

- Holding Company X is the sole shareholder of Companies D, E and F and directly controls these reporting entities.

Company Y, Company A, Holding Company X, Companies D, E and F are all in the control structure. This means they’re all members of the business group.

Companies B and C are minority shareholders of Holding Company X. This means they aren’t members of the business group because they:

- own less than 50% of the shares in Holding Company X

- don’t control Holding Company X or the reporting entities Companies D, E and F.

Who are the members of the reporting group

The business group will automatically be a reporting group because there is one or more reporting entities within it.

The members of the reporting group are Company Y, Company A, Holding Company X, Companies D, E and F.

Who are the eligible members

The eligible members in the business group are all companies besides Company Y. This is because they’re all:

- not controlled by any other member that provides designated services

- a resident body corporate or registered foreign company in Australia.

Who can be a lead entity

Company A and Holding Company X could be lead entities, as they both:

- are eligible members

- have the authority, including by consent, and capability to develop and maintain the group’s AML/CTF policies

The reporting group will then have to ensure a lead entity is in place within 28 days by either:

- all eligible members (all members except Company Y) agreeing in writing on either Company A or Holding Company X being the lead entity

- Company Y appoints the lead entity in writing.

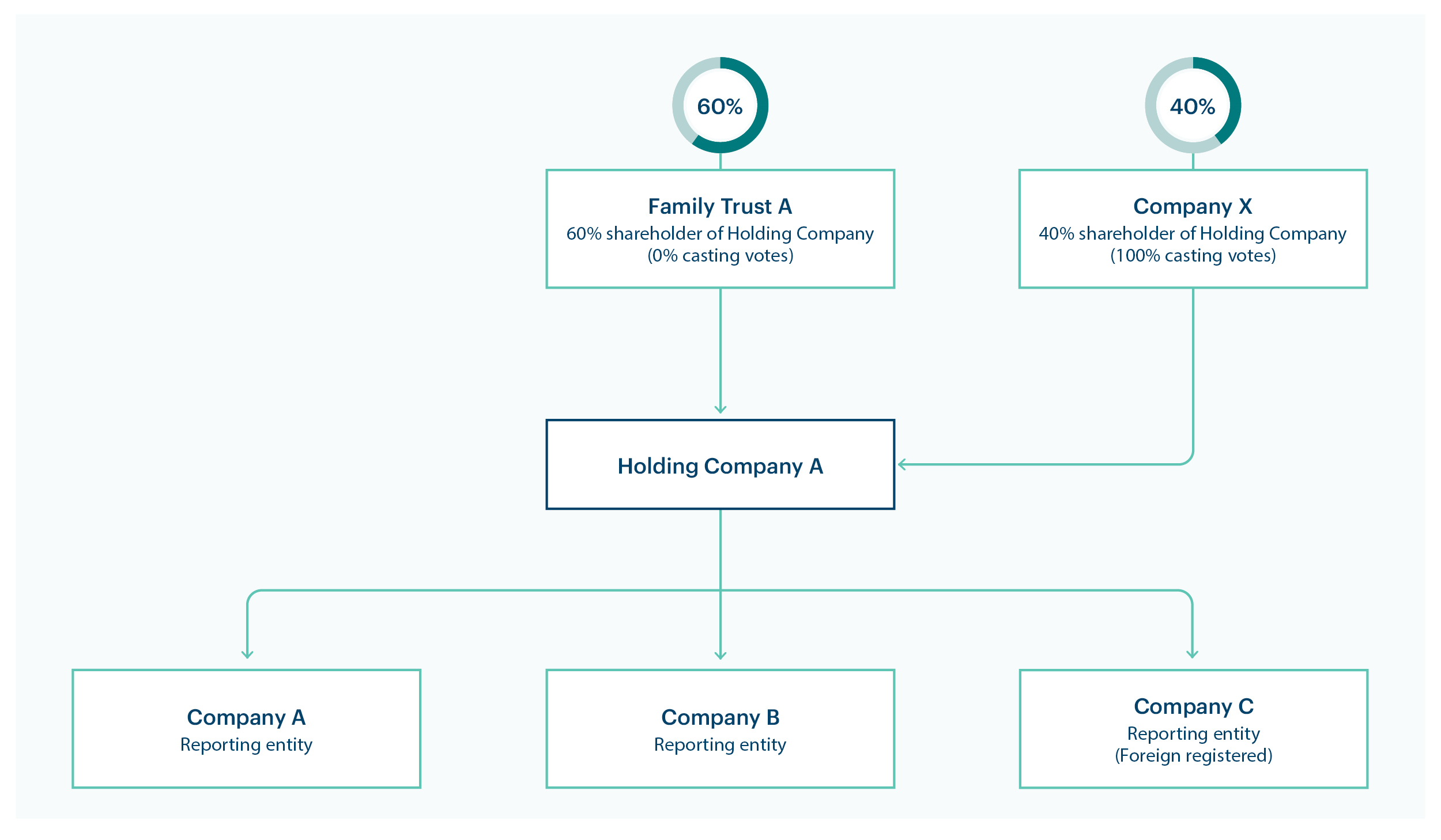

Example: voting power control

All the companies above are incorporated in Australia, except for Company C. Company C is a foreign registered reporting entity and provides designated services overseas through its own office.

The above group are deciding who’s in the business group that can be a reporting group. They’re also trying to determine who the eligible members are and who lead entity could be.

Who are the members of the business group

They break down their structure in the following way:

- Company X controls Holding Company A. While they have only 40% of the shares, they can cast 100% of votes at a general meeting.

- Holding Company A is the sole shareholder of Companies A, B and C. Therefore, Holding Company A has control of these reporting entities.

- Company X, Holding Company A, Companies A, B and C are within the control structure and are therefore all members of the business group.

Company C isn’t registered in Australia and provides designated services from their office overseas. They meet the geographical link requirement criteria, because they are a subsidiary of Holding Company A.

That means they are a reporting entity in Australia and have obligations under the Act.

Learn more at geographical link requirement.

Although Family Trust A is a majority shareholder of Holding Company A, they have no control. They are not in the business group, because:

- they don’t have any casting votes

- they can’t control the board

- they can’t make decisions about the financial and operating policies

- their share capital gives them no right to participate beyond distributions of profit or capital.

Who are the members of the reporting group

The business group will automatically be a reporting group because there is one or more reporting entities within it.

The members of the reporting group will be Company X, Holding Company A, Companies A, B and C.

Who are the eligible members

All entities in the business group besides Company C are eligible members. This is because they’re both:

- not controlled by any other member that provides designated services

- a resident body corporate or registered foreign company in Australia

Who can be a lead entity of the reporting group

Company X and Holding Company A could be lead entities, as they both:

- are eligible members

- have the capability and authority to develop and maintain the groups AML/CTF policies.

The reporting group will then have to ensure a lead entity is in place within 28 days by either:

- all eligible members agreeing in writing on either Company X or Holding Company A being the lead entity

- Company X appoints the lead entity, in writing.

Related pages

This guidance sets out how we interpret certain Australian legislation, along with associated Rules and regulations. Australian courts are ultimately responsible for interpreting these laws and determining if any provisions of these laws are contravened.

The examples and scenarios in this guidance are meant to help explain our interpretation of these laws. They’re not exhaustive or meant to cover every possible scenario.

This guidance provides general information and isn't a substitute for legal advice. This guidance avoids legal language wherever possible and it might include generalisations about the application of the law. Some provisions of the law referred to have exceptions or important qualifications. In most cases your particular circumstances must be taken into account when determining how the law applies to you.