Our annual money laundering update details what channels and threats are influencing Australia’s money laundering environment.

On this page

- Enduring channels and threats

- Technological innovation and changes in the regulatory landscape

- Newly regulated entities

- Growth of illicit tobacco

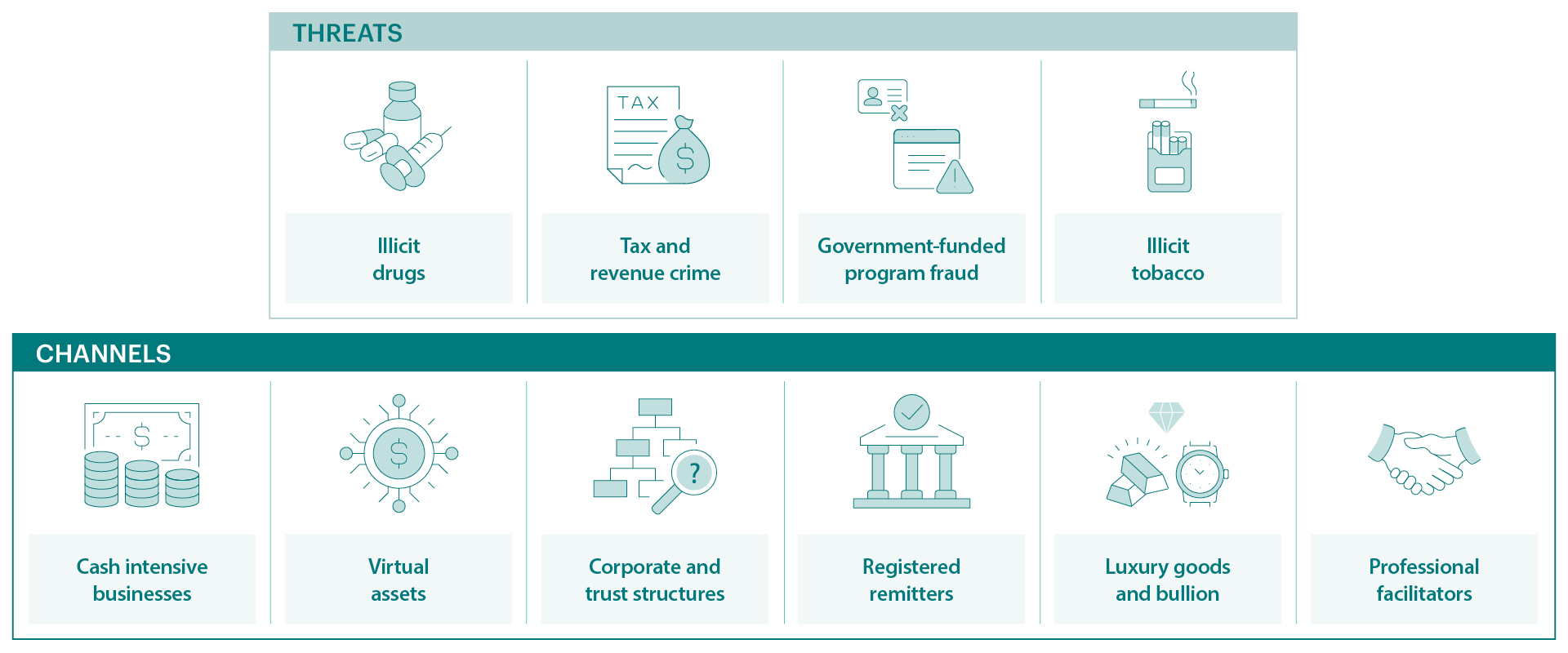

Core channels and threats identified in the Money laundering in Australia national risk assessment 2024 (NRA) remain the same. However, they’re being exploited in increasingly complex, interconnected and transnational ways.

This update outlines enduring channels and threats since the NRA was published. It reflects changes in the broader criminal, economic and regulatory landscape that shape opportunities for exploitation by criminals in this environment.

Enduring channels and threats

Technological innovation and regulatory changes

It’s highly likely Australia’s ML environment will continue to evolve in response to technological innovation and changes in the regulatory landscape, combined with existing criminal methodologies.

While the core risk channels and threats identified in the NRA remain, partner agency and industry data indicate these channels are converging and being exploited in increasingly complex and transnational ways.

This assessment draws on stakeholder input, strategic intelligence and external indicators provided by Commonwealth, state and territory agencies and industry partners. It also highlights where vulnerabilities are most likely to emerge.

Artificial intelligence

Advances in artificial intelligence (AI) and related technologies will broaden risk rather than act as a discrete channel for ML going forward. AI and emerging technologies continue to intensify the ML environment. AI is increasingly utilised for:

- identity fabrication and impersonation

- fake documents

- laundering scam proceeds.

ML impacts multiple channels. Several contributors assessed that AI may both enhance existing professional facilitation channels and, in some cases, reduce the need for traditional facilitators by:

- automating obfuscation techniques

- enabling sophisticated laundering methods with lower barriers to entry.

This is expected to increase exposure to exploitation in areas such as cash‑intensive businesses, corporate and trust structures, and trade‑based laundering, where scale and complexity already present supervisory challenges.

Agencies report growing awareness of criminal actors using AI‑enabled tools to scale activity. It’s used to obscure illicit origins and evade detection, particularly when layered across existing high‑risk channels.

AI is expected to increase the efficiency and sophistication of:

- identity fraud and realistic fake documents

- impersonation used to access financial and non‑financial systems

- transaction structuring and laundering typologies that mimic legitimate customer behaviour

- communications to support account misuse

- trade‑based schemes and shell entities that appear to be legitimate businesses.

Decentralised finance and offshore virtual asset services

The ML risk associated with decentralised finance (DeFi) and offshore virtual asset service providers (VASPs) has evolved as the structure of digital value transfer has shifted beyond traditional points of regulatory control. DeFi platforms and offshore VASPs are increasingly used to move and layer value through environments where supervisory reach is limited. This is particularly common through virtual asset activity and transactions conducted wholly outside of domestic jurisdiction.

Reduced transactional transparency, rapid settlement and cross‑border fragmentation are weakening attribution and traceability.

This shift reflects structural features of the current operating environment. Regulatory obligations for VASPs are concentrated on fiat on‑ and off‑ramps. Fiat on‑ and off‑ramps are services that allow conversion of traditional money into digital assets and vice versa. This leaves gaps in visibility for crypto‑native transactions and decentralised activity.

International factors

International differences in customer identification, reporting and information‑sharing standards further limit the ability to trace value flows across borders. Market trends toward decentralised and offshore platforms reinforce these conditions. Activity moves into systems that are opaque and more difficult to disrupt.

These developments are also reshaping where ML risk accumulates. The growing integration of DeFi and offshore VASPs with other high‑risk services reduces reliance on reportable conversion points. It also creates blind spots for detection and supervision. Going forward, this is expected to move laundering activity into less visible parts of the financial system, increasing the challenge of maintaining effective oversight.

Financial channels and criminal activities

Greater convergence across high‑risk designated services is highly likely to remain attractive for criminal exploitation. This includes situations where services such as remittance, VASPs, bullion dealing and cash are offered together.

Long-standing networks provide ML services to a range of serious and organised crime groups. These ML networks (MLNs) are capable of rapid conversion between virtual assets and international transfers with limited reliance on further providers or stages.

MLNs’ ability to structure, disguise and accelerate laundering activity is supported by their capacity to circumvent regulated on- and off- ramps from fiat currency. MLNs exploit differences in:

- regulatory obligations

- transaction thresholds

- compliance triggers across services.

Convergence across multiple designated services increases risk and potential harm by hiding criminal activity. This is likely to remain an attractive pathway for financial exploitation.

Newly regulated entities

From 1 July 2026, anti-money laundering and counter-terrorism financing (AML/CTF) obligations apply to designated services provided by the following businesses:

- real estate professionals (such as real estate agents, buyer’s agents and property developers)

- conveyancers

- dealers in precious metals, stones and products

- lawyers

- accountants

- trust and company service providers

- additional virtual asset-related service providers.

Many of the entities covered by the new regulation have been identified as high or very high-risk of being exploited for ML.

Regulation of these new entities should improve our understanding of:

- high‑risk entities

- service convergences

- the movement of illicit funds.

Growth of illicit tobacco

The sale and supply of illicit tobacco is driven by demand and the high profitability of this crime type. It generates billions of dollars in proceeds that are laundered through Australia’s financial system. The threat environment has continued to evolve since 2024.

Illicit tobacco has increased in volume and criminal groups are becoming more sophisticated when moving their illicit financial proceeds. While it has been previously assessed as a medium ML threat, illicit tobacco is rapidly accelerating and approaching a higher ML risk rating. Being driven by high market demand and profitability, it’s also increasingly being linked with multiple high-risk channels including cash-intensive businesses and remittance providers.

Serious and organised crime syndicates

This market continues to be underpinned by transnational serious and organised crime syndicates, including organised crime groups and outlaw motorcycle gangs (OMCGs). Efforts by transnational serious and organised crime groups to assert control over the growing illicit tobacco market have escalated in recent years. This has led to:

- widespread arson attacks

- multiple homicides

- other violent assaults.

Domestic demand

Domestic demand will almost certainly remain high and organised crime groups will continue to participate in trafficking and supply activities, given the high profitability of doing so. Addressing this threat requires sustained national disruption efforts to:

- reduce the availability of illicit products in the community

- target associated violent criminal activity and effectively

- detect and disrupt illicit financial flows.